The Solution to Type II Inflation Risk is UBI

A Capital-Consumption Theory View

Jack Dorsey recently tweeted that hyperinflation is coming.

Many responses have been a one-word “No.” Ignoring the strawman argument of “No, 5% inflation is not hyperinflation,” the conditions and mechanisms of hyperinflation are worth examining, if for no other reason than to assure ourselves that we are not, in fact, headed towards the possibility of hyperinflation.

We can, very broadly, divide most current thinking into two camps. One is the “more stimulus” camp, including those such as Claudia Sahm, Noah Smith, Paul Krugman, and Stephanie Kelton. On the other side is the “less stimulus / inflationary risk” camp, including those such as Larry Summers, Jack Dorsey, and Peter Schiff.

For the most part, both camps fail to examine the underlying paradigm — that the goal of economic management is to prevent unemployment and extended economic downturns, on one hand, and inflation, on the other hand. And, therefore, that we should avoid providing too little stimulus to the economy, which might cause an extended and unnecessary downturn; but, on the other side, we should also avoid providing too much stimulus to the economy, and triggering inflation. This dichotomy is enshrined in the Fed’s “dual mandate,” and shapes much of Federal Open Market Committee (FOMC) discussion, which is often characterized by an examination of the balance between “upside risks” and “downside risks.”

As I write about in another article, traditional fiscal policy and traditional monetary policy are becoming ineffective. It was never the plan of FOMC or anyone else to reach the point of 107% government debt-to-GDP and a 96% increase in the base money supply within the last 2 years, but this is where we now are.

If you’re in the “more stimulus / don’t worry about inflation” camp, how much further do you go? And when does inflation eventually hit, as everyone seems to agree that it eventually does? If 107% debt-to-GDP and a 96% increase in the base money supply isn’t enough, is twice that amount enough? What amount triggers inflation?

As Noah Smith points out in a recent article, no one seems to have an answer to this question.

If you’re in the “less stimulus / worried about inflation” camp, what do you do when a reduction in stimulus causes the economy to contract? What stops the contraction? And why is a contraction in the economy necessary in the first place?

In the context of the current one-dimensional paradigm, what do you do when problems close in from both sides, with reasons to worry about “downside risk” and reasons to worry about inflation risk both increasing? Who’s right? You can’t both increase stimulus to prevent contraction and also decrease stimulus to prevent inflation. Or can you? How do we resolve this dilemma?

To resolve the dilemma, we need to distinguish between 1) balance in government finances, and 2) (capital-consumption) balance in the economy, while recognizing the different functions of capitalists in the economy vs. everyone else (consumer-workers).

Currently, the top 10% of wealthy Americans control 90% of the assets, while 90% of Americans control only 10% of the assets.

The existence of these assets, for the most part, is a potential benefit for the economy. Assets such as stocks and bonds are ultimately the funding mechanism for real investment into productivity-enhancing real capital and increased productive capacity. In return, the owners of the assets gain capital income, a portion of the increased productivity that real capital accumulation enables.

In contrast, those without assets (the consumer-workers) must, directly or indirectly, rely on labor income to meet their consumption spending needs.

The problem here stems from what I will call the Automated Factory Paradox, which was described by Alan Watts, and is mentioned, in the UBI community, by Alex Howlett and Geoff Crocker. In Alan Watts’s version, a businessman builds a wonderful automated factory, lays off all his workers, and then turns around to find that there are no customers to buy the products of his factory, because they’re all out of work.

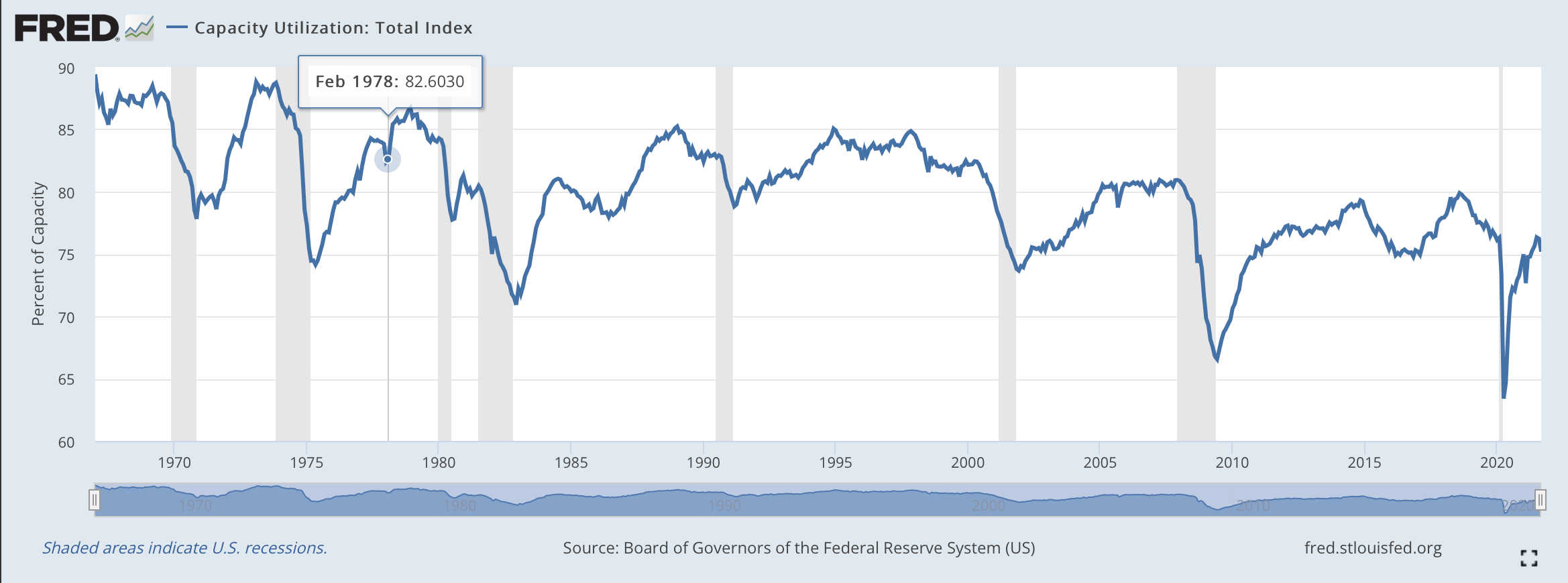

To the degree that labor income is insufficient for the 90% of consumer-workers to purchase the full production that the economy can produce and fully utilize the productive capacity of the economy, the result is widespread under-utilization in the economy. This under-utilization is visible in low capacity utilization (chart below). It also encompasses under-utilization of capital, which is seen in low long-term market interest rates, and under-utilization of labor, which is seen in stagnant wages since around 1980.

The capitalists are unable to help in this regard (in consumption and capacity utilization), because their income mostly goes to investing in increased capacity, which while potentially a benefit in terms of increasing productivity and increasing capacity, only worsens Automated Factory Paradox.

The resulting frustration of real investment due to insufficient consumption spending causes financial capital to back up in a condition of over-supply, causing a “savings glut” and low long-term market interest rates.

Low interest rates then encourage a high level of government borrowing, while the drag on the economy caused by insufficient labor income in the hands of the consumer-worker seems to necessitate “economic stimulus” through “fiscal policy.”

In an economy suffering from capital-consumption imbalance, at least three distinct problems stem from the single root cause. We’ve talked about 1) unbalanced government finance. Additionally, the “savings glut” and low interest rates lead to 2) asset bubbles, which help to hold up spending through the wealth effect, but in an unstable fashion which is vulnerable to asset crashes. Finally, you have 3) debt expansion, which also holds up spending, but also in an unstable fashion which is vulnerable to debt shocks.

Where does the risk of inflation or hyperinflation come from, if it exists? We saw above that capacity utilization is near century lows. This would seem to rule out broad capacity-constraint inflation, if utilization is very low across the entire economy. However, there may exist a risk of inflation due to loss of faith in the currency, which is driven by an excess of idle, stagnant capital at the top of the economy, our “savings glut.”

In the presence of asset bubbles and low interest rates, this excess, idle capital at the top steadily loses productive outlets for investment. Equities begin to seem marginal as investments due to their high valuations. The same with real estate. And Treasury bonds, which are now yielding negative real interest rates, seem guaranteed to lose money for the long-term holder.

In this situation, and in the presence of increases in the base money supply, etc., there will be an incentive for investors to move their money savings into inflation hedges like gold, Bitcoin, real estate, and commodities. All of which will reduce money demand, measured in the length of time for which investors are willing to hold money. This includes the level of debt which investors and businesses are willing to keep, which can be considered a negative holding period for money. The result is an increase in inflationary pressure, which may worsen if the level of inflation currently being experienced persists.

It’s important to understand here that the inflationary risk comes not from an overheated economy, as suggested by the one-dimensional paradigm which often goes unexamined. Rather, the risk comes from excess, idle capital at the top of the economy, which generates the basis for potential unstable capital flows out of the currency. Counterintuitively, insufficient consumer spending at the bottom of the economy plays a key role in causing this excess, idle capital, by stifling real investment into productive capacity as a productive outlet for capital.

We can say that the economy suffers from an inflationary top and a deflationary bottom.

The sustainable solution, then, is to reduce “stimulus” at the top of the economy while increasing “stimulus” at the bottom of the economy. A monetary UBI, similar to stimulus payments that have gone out during the COVID crisis, but on a continual basis, should be instituted at a level of $1200 per month, combined with a decrease in QE and traditional monetary policy, withdrawing money from the inflationary top. Additionally, taxes on corporations and the wealthy should be increased in order to re-balance the fiscal deficit over time and shore up the stability of government finances.

If done correctly, a re-direction of stimulus to the bottom of the economy and away from the top will revive consumer spending and the real, productive economy, while replacing the unstable debt and asset bubbles currently holding up the economy, and also allow for the re-balancing of government finances to a more sustainable path.

Some of this went over my head, but I have a couple thoughts: I think the main problem with UBI is that it ignores human nature. You will wind up with a growing percentage of the population that is content to stay home collecting their UBI, watching Netflix, eating fast food and smoking weed. Note for instance, the reluctance of many to rejoin the workforce even after extended UE benefits ran out.

Most unskilled labor is dreary and monotonous and given the choice between being poor while not working but collecting UBI on the one hand, or being slightly less poor while working a boring dead-end job on the other, hordes of workers will simply opt out. As such, instead of a national work ethic, a lift-yourself-up-by-the-bootstraps mentality, a spirit of ambition, striving to get ahead, to better oneself, eagerly seizing opportunities, achieving the American dream, and so forth, you will inadvertently be encouraging passivity, dependency, and resignation to one's lot in life.

I'm not a religious man, but I find much collective wisdom of the ages is contained in ancient literature: "The person who labors, labors for himself, For his hungry mouth drives him on." (Proverbs 16:26) And Paul wrote, "if anyone will not work, neither let him eat." (2 Thess. 3:10).

I dropped out of high school and worked many minimum wage jobs. I was motivated because there was no option of free government money. It was work or starve. That's how you develop a work ethic. You're not going to develop that on your own if the government is conditioning you to depend on handouts. Because of that work ethic, when a business opportunity arose, I recognized it, seized the day, worked my a$$ off and went from being hopelessly in debt with no future prospects to being debt free with a solid income, savings in the bank, investments, retirement account, and even being in a position to provide financial help to others. Now instead of being a burden on the taxpayers, I am cutting quarterly checks to Uncle Sam.

So you can chalk me up as being in the Peter Schiff camp. Economic downturns should occur. They should be brief. They should provide creative destruction, killing off weak businesses and freeing up resources for more productive uses. The notion that we could engineer our way to a system in which no downturns occur is seductive, but misguided. There's no such thing as a free lunch and nothing goes up in a straight line. Businesses and individuals should both be encouraged to save for a rainy day and understand that when that day comes there will not be a social safety net to swoop in and save them from all their bad decisions and shortsighted excesses. And for those who fall through the cracks? That's where charity comes in.